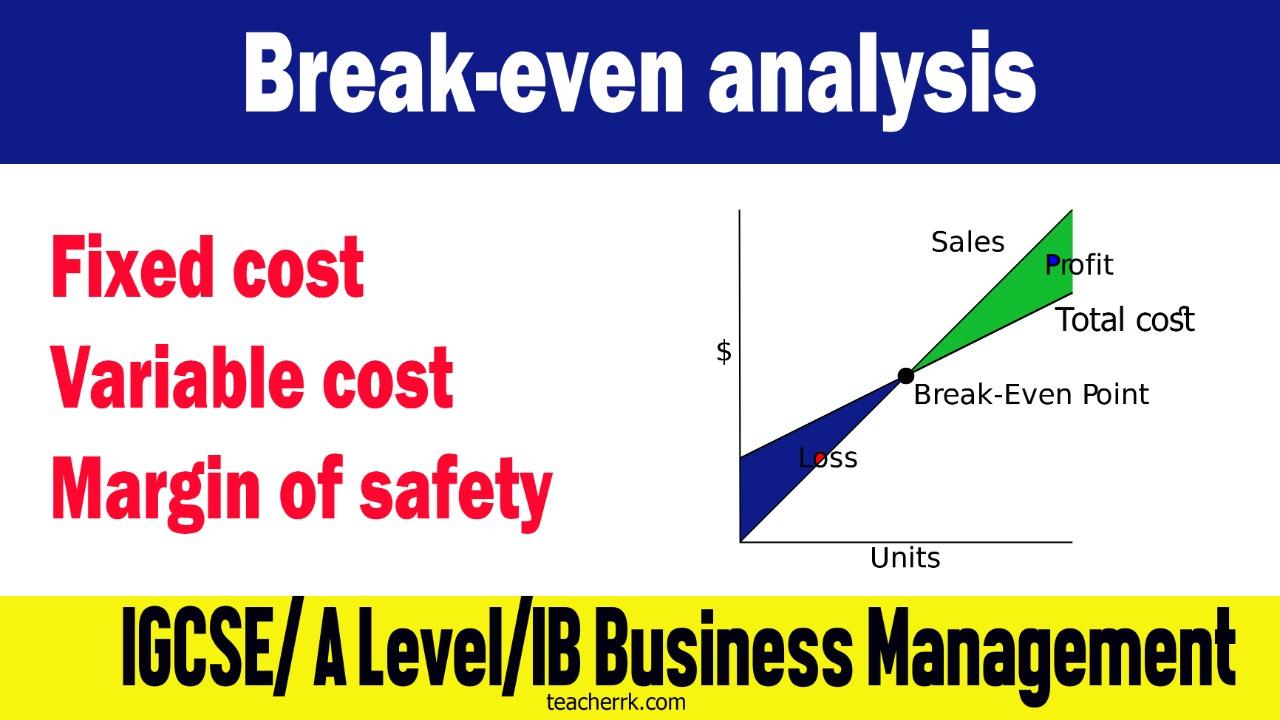

- Break even quantity

- Break even revenue

- Margin of safety

- Profit

You are given the following cost and revenue details

| Business A | Business B | |

| Fixed cost | $ 20 000 p.a. | $ 40 000 p.a. |

| Variable cost | $120 per unit | $ 60 per unit |

| Selling price | $ 200 per unit | $ 100 per unit |

| Current output (Annual) | 400 units | 1200 units |

Questions:

- Identify five assumptions of break even graph [ 2 marks]

- Calculate unit contribution for both Business A and Business B [ 2 marks]

- Calculate break even quantity for both Business A and Business B [ 4 marks]

- Calculate break even revenue ($) for both Business A and Business B [ 4 marks]

- Calculate margin of safety (units) for both Business A and Business B [ 2 marks]

- Calculate profit at the current level of output for both Business A and Business B [ 4 marks]

- Calculate the number of units to be sold to make 20 % more profit from the current level of profit [ 6 marks]

1 thought on “Break-even analysis – Worksheet 29: Meru Limited”

Comments are closed.